By Julian Nabil and Sara Mohamed

As the end-of-year deadline approaches, a thorough going-over of the demand and supply is fundamental to assess the status quo. Therefore, Invest-Gate puts the Egyptian real estate sector under the spotlight, examining the current conditions of the two crucial poles of the industry, while laying hands on the trending tactics used by property developers to excel and ace the market circumstances.

Demand Volume

Egypt’s demographics had been the main driver of residential demand, as is the case in many high-density countries, with the population growing around 1% to reach roughly 98.1 mn, excluding expats, in 2019, based on official figures by the Central Agency for Public Mobilization and Statistics (CAPMAS).

On the other hand, the property market saw a decline in the volume of demand this year. According to Egypt’s property listing platform Aqarmap, the real estate index recorded 2,810.4 points in the first ten months of 2019, a decline of 9.5% from the 3,108.4 points registered in the corresponding period last year.

On the other hand, the property market saw a decline in the volume of demand this year. According to Egypt’s property listing platform Aqarmap, the real estate index recorded 2,810.4 points in the first ten months of 2019, a decline of 9.5% from the 3,108.4 points registered in the corresponding period last year.

“This is mainly dragged down by buyers’ slowing affordability, a near saturation in the upper-middle- and upper-class demand, alongside the undersupply of affordable units by the private sector,” according to Aqarmap Business Development Manager Ahmed Abdel-Fattah.

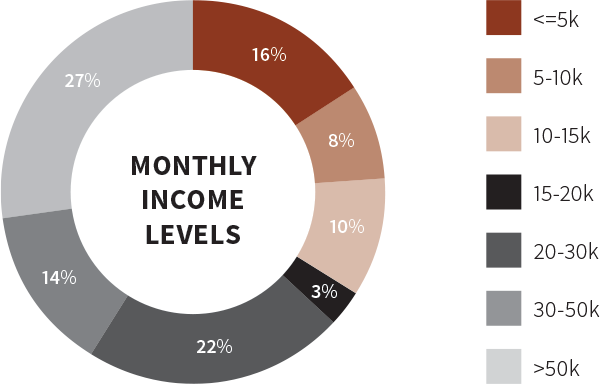

Based on the FY 2018/19 estimates of the Arab African International Securities (AAIS), the overall demand in Cairo and Giza is mostly dominated by middle- and low-income classes at 71% and 14.2%, respectively. | According to Invest-Gate R&A’s report, titled “The Purchasing Power Report 2019,” a solid majority (70%) of potential purchasers shop for properties with a maximum price tag of EGP 1.5 mn this year. | In contrast, market experts see the high-end residential units remain to be an integral part of the private housing supply, leaving the larger chunk of those falling below the upper-income class mainly served by the government’s offerings only. |

Buyer Demographics & Preferences

In 2019, a whopping of 63% of willing purchasers fell into the bracket of EGP 20,000 to over EGP 50,000, while only 24% of those who can afford to buy units earn below EGP 10,000. Besides, 71% of prospective investors looked for apartments, while only 23% preferred villas, according to Invest-Gate R&A’s recent report.

On another note, a mass influx of clients are still bound to buy real estate for primary residence purposes, tending to downgrade their requirements and preferences as property values spring up and purchasing power slows down, Mena Group Founder Fathallah Fawzy tells Invest-Gate.

JLL Country Head of Egypt Ayman Sami argues that unit price hikes fueled the demand of actual home seekers for rentals as an internal solution this year. However, 78% of potential buyers still prefer to purchase rather than rent, 71% of which are willing to seal deals in the present juncture but are still scouting for satisfactory properties, Invest-Gate’s latest study revealed.

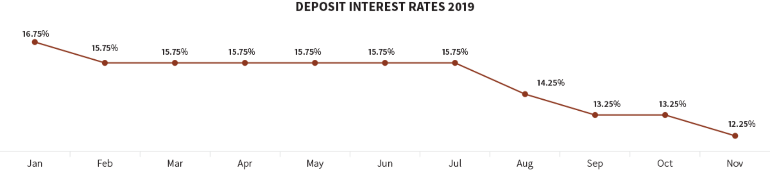

Sami notices more inclination toward the resale market as 2019 approaches its end, mainly driven by the declining interest rates since February, with the overnight deposit rate reaching 12.25% in mid-November.

As for the second-home market, Mohamed Hammad, managing director of Property Finder, previously told Invest-Gate that it saw less demand this year compared to prior times, which had witnessed booming sales, mainly due to the fact that rates of coastal houses have been proliferating at a higher pace in 2019, thereby weakening purchasing power in the vacation market. This ought to the low-income levels of Egyptians, which do not reciprocate with these accumulations. He revealed that the upper-income group takes up the lion’s share of targeted clientele, hence sales for this year’s summer.

The supply of homes on the Egyptian market had a different scenario … Read pages 18-21 at Invest-Gate’s December issue to know all about it!